It’s no secret that the housing market is shifting. In fact, high home prices and low inventory have made it challenging for potential buyers to even get into the market. However, this is a great time for homebuyers, but because there are so many common misconceptions of buying your first home, let’s dive in with a little education to clear it all up. So whether you’re looking to buy your first home or just curious about what goes on behind closed doors at closing time, keep reading!

Misconception #1: You need a 20% down payment in order to buy a house.

A down payment is the amount of money you pay upfront to buy a house. The rest of the cost is usually financed over a period of years (typically 30 years) in monthly mortgage payments.

Most people believe that you need to come up with 20% for the down payment on your house when in reality you can put down as little as 3%. If you purchase with less than 20%, then you may have to pay for

Private Mortgage Insurance (PMI) to protect against any losses if things don’t go as planned and you default on your mortgage loan.

The best time to buy a home is when you are

financially ready, which means having saved up enough cash for a down payment and closing costs (anywhere between 2-4% of your total purchase price). If you have good credit, it’s also helpful to have some savings in the bank so that you don’t have to rely on your credit card for emergency funds or new furniture for the house.

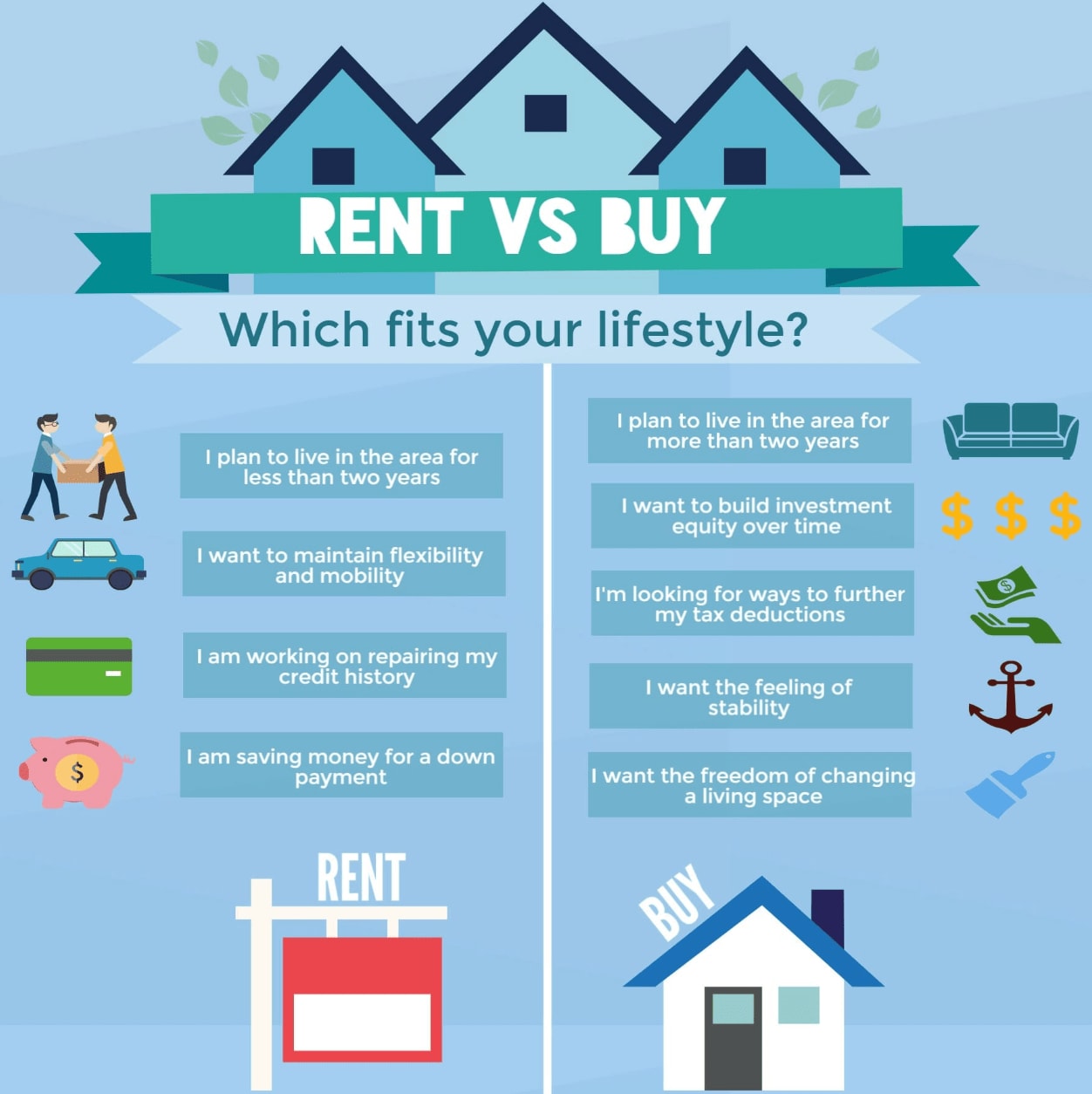

Misconception #2: It’s actually cheaper to rent than buy.

Renting is expensive.

Did you know that the rent you pay ends up paying for someone else’s mortgage? Every time you pay rent, it’s a down payment on someone else’s house. You’re literally investing in someone else’s home and their property value, instead of building up equity in your own place.

And that’s not all: Rent is typically higher than a mortgage with no equity growth. It doesn’t matter if you’re living in a nice neighborhood or an undesirable one—if you’re paying rent, you’re essentially paying for the privilege of living somewhere with no appreciation potential. That means that every month spent on rent is a month spent on something that will never get better—you’ll never see any return on investment beyond the initial cost of signing the lease agreement.

And then there are move-in fees—another way landlords can charge you more than they should! Move-in fees are usually pretty high and often go towards things like repainting walls or replacing light fixtures; things that are supposed to be included in your security deposit but instead come out of pocket at move-in time (which means they’re not coming back).

Buying a house is a good investment, and one that will likely grow in value over time as long as you maintain it well and keep up with the maintenance costs and repairs. This means buying a home can be an excellent way to build equity, keep yourself protected from rent increases or evictions, enjoy tax advantages (such as deducting mortgage interest), and pass along wealth to your family when you sell it someday—but only if you actually purchase real estate instead of renting!

Misconception #3: The more earnest money you put down, the more likely the sellers will accept your offer.

When you’re putting in an offer on a home, it’s easy to get bogged down in the details of the contract—but here’s what you need to know:

Putting down earnest money is not directly correlated with getting your offer accepted.

What does that mean? It means that putting down earnest money is just one part of the process, and it shouldn’t be the only thing you focus on. When you’re writing your offer, think about what would make sense for both the seller and the buyer. If their kids are graduating from high school in June, don’t write an offer asking to move in April 1st—that would be too soon! Instead, focus on contingencies like inspection dates and final walkthroughs. The less contingencies you ask for, the better your chances are of getting your offer accepted!

A little education goes a long way!

Those were just a few of many common misconceptions of home ownership but If there’s anything that stuck with you after reading this article, let it be this: Buying your first home can be scary but the more educated you are on the topic the more confident you will be in your decision.

Let’s connect!